|

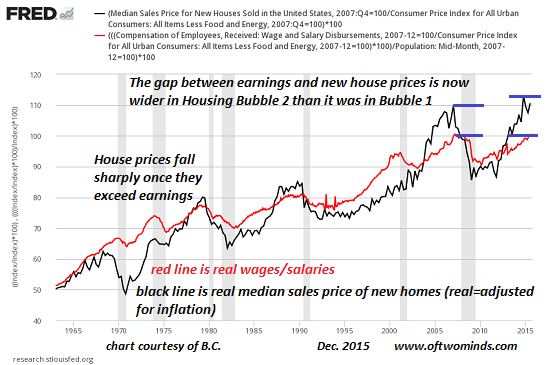

Housing Bubble 2 in One Chart by Charles Hugh Smith "Now the gap between real house prices and real earnings is even wider than it was in Housing Bubble 1."

We know two things about housing bubbles: they always pop, with devastating consequences, and apologists and pundits always deny housing is in a bubble. Courtesy of longtime correspondent B.C., we have a chart that not only identifies housing bubbles but explains why they inevitably collapse. We have become so accustomed to housing being propped up with 3% down-payment FHA loans, foreign buyers paying with cash and Fed-favored financiers buying 10,000 homes to rent to former homeowners that we tend to forget that in the longer term, housing sales depend on buyers with enough income to pay the mortgage, property taxes, repairs, etc. This chart reveals the tight correlation between real (i.e. adjusted for inflation) new house sales prices and real wages/salaries. House prices fell again in the late 1970s when they briefly exceeded the growth of earnings. An extended period of housing prices soaring above earnings in the late 1980s was followed by a slump in housing in the early-to-mid 1990s. Housing (black line) is relatively cheap when it is well below earnings (red line). Housing Bubble 1 is clearly visible as house prices skyrocketed far above earnings in the 2004-2008 period.

Now the gap between real house prices and real earnings is even wider than it was in Housing Bubble 1. To expect anything different is unrealistic and highly dangerous to one's financial well-being.

|

| © 2006 - 2022. All Rights Reserved. |