|

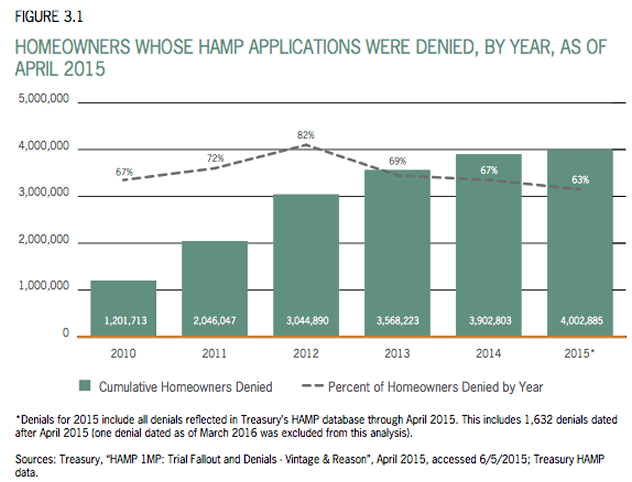

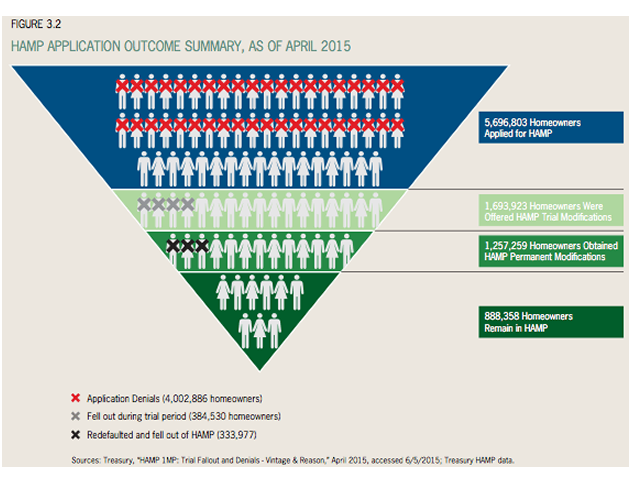

Watchdog Claims the Treasury & Servicers Are Not Doing Enough on Loan Mods The Treasury Department rebutted a watchdog's claims that it hasn't done much to lower high Home Affordable Modification Program denial rates. The Special Inspector General for the Trouble Asset Relief Program recently renewed its criticism of the high denial rate in Hamp. Paperwork backlogs are one root cause of the problem, according to the watchdog, along with from insufficient Treasury oversight and servicer calculation errors. The Treasury counters that things are better than they once were. "We have seen significant improvement in servicers' compliance with program guidelines, including proper evaluation and denial decisions," said Mark McArdle, chief of the Treasury's Homeownership Preservation Office in a July 29 letter. McArdle noted that there has been improvement in HAMP denial rates since 2012. That year, Treasury introduced HAMP Tier 2, which allowed a more flexible debt-to-income ratio. McArdle also noted that documentation has been simplified over time, and that Treasury recently introduced a Streamline HAMP program. HAMP is part of the government's Making Home Affordable initiative. Data from SIGTARP and Treasury show denials on average fell sharply to 69% in 2013 after peaking in 2012 at 82%. The average as of April was 63%. Other statistics show cumulative HAMP denials have climbed significantly over time, increasing by 1 million since 2012. The top reasons applications get denied are incomplete applications and insufficient income, according to SIGTARP. According to SIGTARP, the top servicers it singles out for criticism had higher-than-average denial rates of 70% to 80% — notably Citi, Bank of America, JPMorgan Chase and nonbank Ocwen. But these companies took issue with the government watchdog's analysis of Treasury statistics on the program. "Chase has achieved the Treasury's highest overall MHA compliance scorecard rating for six of the last seven quarters. We believe today's reported findings are based on an inaccurate analysis of Treasury data," spokesman Jason Lobo said in an email. Citi said its denial rate is lower than what SIGTARP said it is when based on completed customer applications. It also said it is able to process most applications in no more than a few weeks. SIGTARP charges that backlogs at some servicers are more than a year long. The backlog of loan modification requests at some mortgage servicers is so bad that at one servicer the pile-up of paperwork caused a storage room floor to buckle, SIGTARP said last year. (That servicer, SunTrust, had no immediate comment Thursday.) "Citi has consistently approved approximately 50% of complete customer applications representing nearly 100,000 HAMP loans. In most cases, Citi provides a decision within 20 days of receiving a complete application," said spokesman Mark Rodgers. The HAMP application pipeline is generally paper-intensive and can be challenging for consumers and servicers alike, but has improved over time, according to Karl Falk, chief executive of consumer-facing mortgage default servicing technology provider ShortSave. When asked why HAMP denial rates are so high, what the cause of this might be and who might be responsible, he said, "If you want my opinion, it's the process, but it's hard to point any fingers in that." Streamline HAMP is one Treasury initiative that appears helpful, according to Falk. "I'd be curious to see if those have higher approvals," he said. But top servicers said that that they felt their success in providing foreclosure alternatives should not be measured by HAMP approvals alone. Although about two-thirds of reviewed applications cannot qualify for a modification under the explicit guidelines of the government programs, servicers are able to help many consumers avoid foreclosure through other avenues, according to Bank of America. "In the end, 83% of more than one million customers whose HAMP applications were reviewed by Bank of America — five out of six — avoided foreclosure," spokesman Rick Simon said in an e-mailed statement. Top HAMP servicer Ocwen said in a statement it also has helped borrowers who did not qualify for HAMP avoid foreclosure though other means. Ocwen said it has addressed some of these consumers' loans with private modification programs. "A significant number of borrowers who did not qualify for a HAMP modification did receive a proprietary modification from Ocwen," John Lovallo, an Ocwen spokesman, said in an e-mail. Ocwen's denial rate is roughly 10 percentage points lower than the three aforementioned banks, according to SIGTARP. Ocwen has a relatively high number of distressed loans in its portfolio. The housing recovery has reduced distress and the need for modification recently. Ocwen Financial at one point failed a test to determine whether it had notified borrowers of missing or incomplete documents for loan modifications in a timely manner, but said it has been working since then to improve its compliance.

|

| © 2006 - 2022. All Rights Reserved. |